Summary

U.S. Property & Casualty (P&C) insurance is a $1T+ market, yet almost one-third of every premium dollar disappears into operations and admin spend. We’re talking of an industry with $77B wage-pool, much of it lost amidst PDFs, phone calls, and spreadsheets.

The result? Lot of grunt work, delayed timelines and billions left on the table.

With context aware foundation models reliably parsing, consolidating and enriching unstructured data, we’re at an inflection point: AI can finally convert insurance’s messiest workflows into scalable, auditable software. In our previous blog, we explored why Accounting is AI’s next big frontier. This time we’ve identified Insurance as another vertical where AI has started making waves already.

It’s Tuesday, 9:12 a.m. when Christine, a commercial insurance broker opens a submission: a regional food manufacturer wants his 8 sites across 6 states insured. Each site means 50+ data fields spread across myriads of documents: loss runs, engineering reports, site plans, cat models. She copy-pastes her way through ACORDs and portals to blast 20 insurance carriers.

At Liberty Farm Insurance, intake clerks triage thousands of applications. David, an underwriter, lives in tabs: email, rating tools, spreadsheets, Policy Admin System (PAS). 5 days to quote; one missed data field turns days into weeks. After endless back-and-forth with Christine, the policy binds. Finally.

Months later, a pipe burst at one of the insured sites starts the claims clock. Similar bottlenecks, different roles. Simple claims close in 60 days, complex ones can take 9 months!

Now imagine the same journey when every document is machine-readable, and every decision is AI-assisted. That’s what we unpack in this blog!

30%+ of P&C insurance premium goes into ops & admin spend

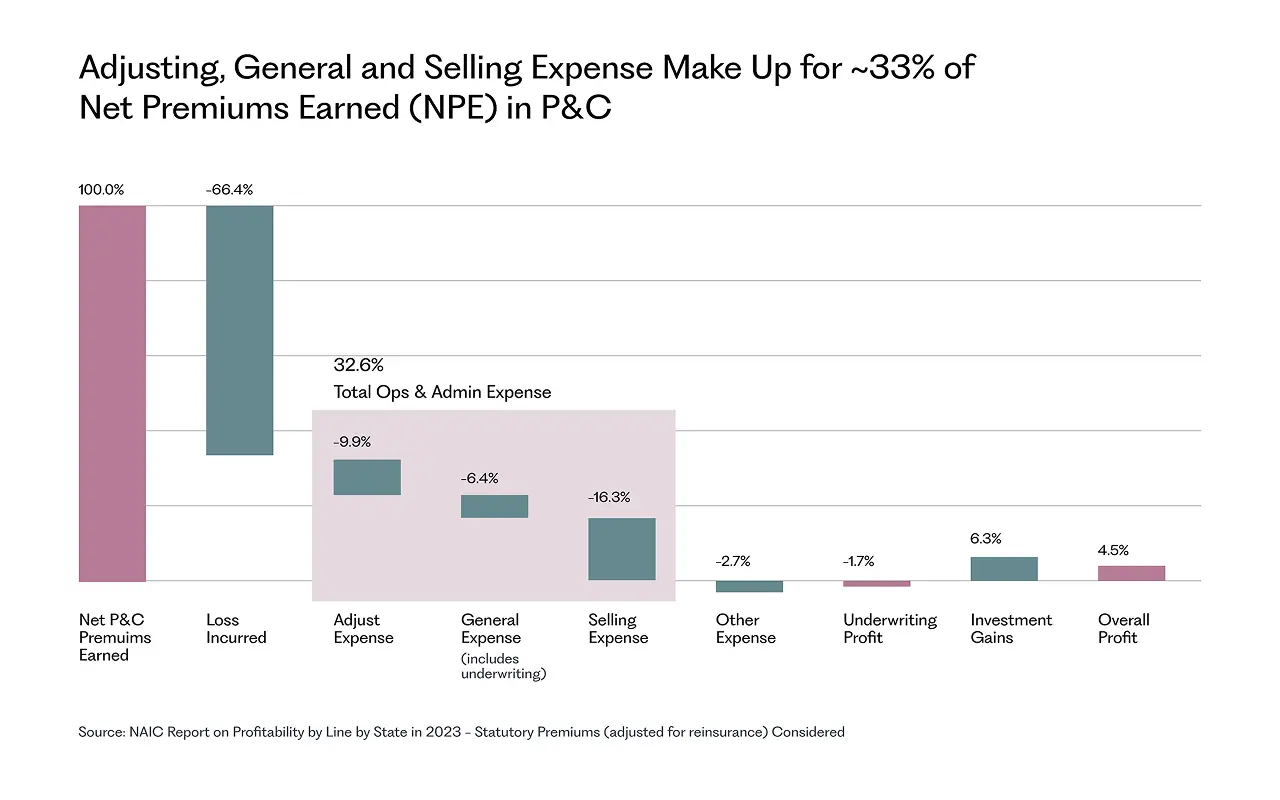

The US P&C earns $1T+ in annual premiums, split 50/50 between personal and commercial lines. At first glance, $1T of premium might sound like a cash machine. But look closer: 66.4% of those premiums go straight back out the door in claims. Another 32.6% gets eaten up by the endless manual workflows that keep the engine running — broker commissions, underwriting costs and claims adjustment expenses. Add taxes, licensing, and fees, and the sector’s underwriting margin slips to -1.7%.

The result? Premiums aren’t the profit center. Insurers actually lose money on underwriting. It’s the invested reserves sitting between premium collection and claim payout that pulls carriers back above water.

And if you dissect the expenses by each line of business, you’d realize — commercial lines beat personal ones by a significant margin.

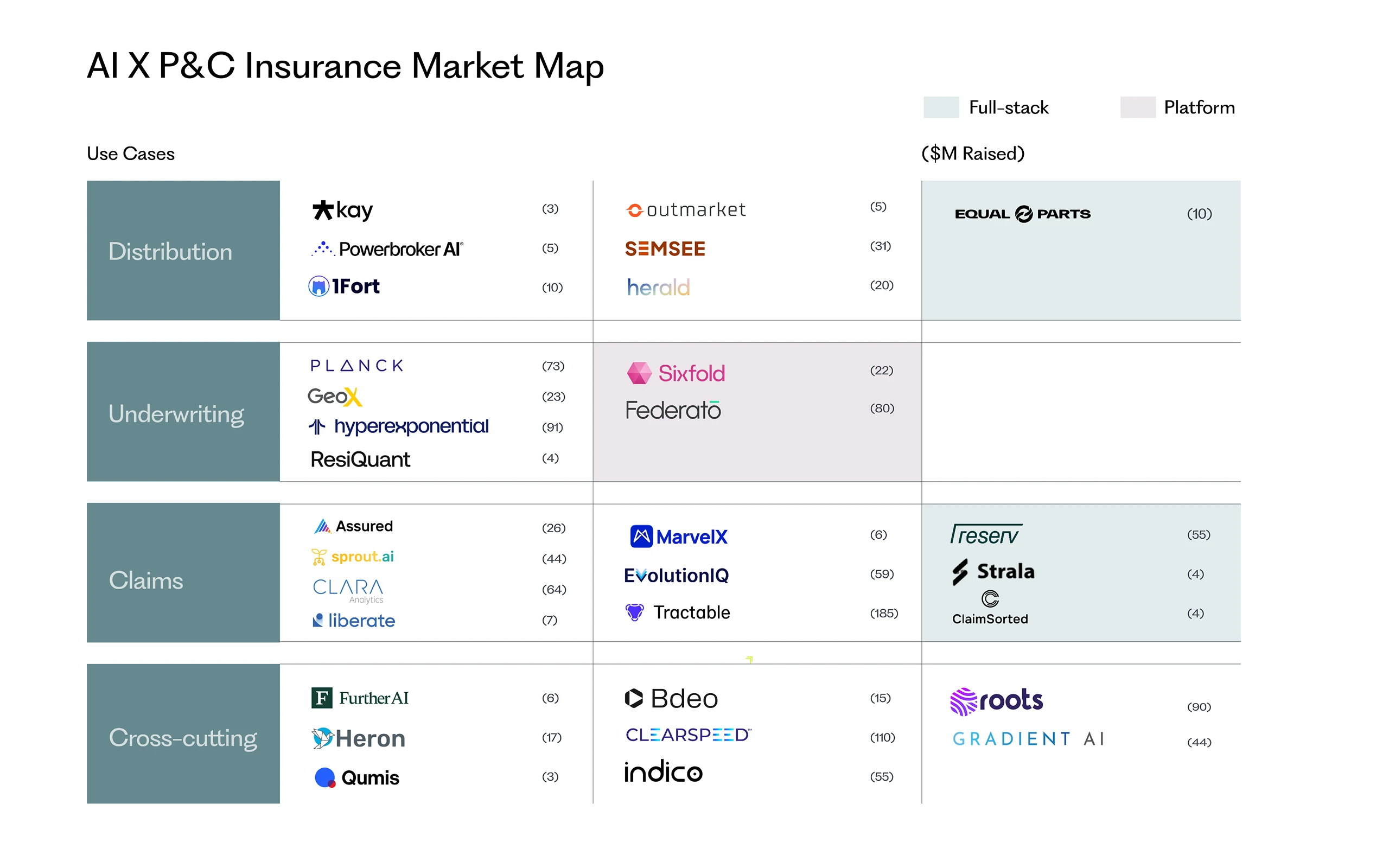

We zoomed into each of the three cost buckets, mapping them against the value chain and getting into the weeds of the market landscape. Commercial insurance is space where multiple stakeholders co-exist. There are ~2600 carriers, ~700 Managing general Agents (MGAs), ~40,000 brokers and hundreds of Third Party Administrators (TPAs). We critically looked at all possible business models that could make sense here — platforms, point-solutions and full-stack plays. From the analysis, three clear opportunities (for each of the three cost buckets) emerged that we’ll unwrap as follows.

Model 1: AI agents for application handling and underwriting

Carriers’ underwriting workflows can be divided across two buckets — core and non-core:

- Non-core (submissions intake & triage):

The job here is to make sense of huge application volumes, lift hit ratios, and route to the right underwriter. These workflows were largely manual until recently, when carriers began desperately hunting for modular plug-and-play agents. We’re seeing multiple tools being picked up by carriers — they have little tech differentiation, but gain brownie points from being adopted by the top 10 carriers — creating a flywheel that attracts more. There are decade old players like Indico Data and AI-first newcomers like Further AI competing for the same prize. - Core (the underwriting workbench):

Carriers view the core risk assessment engine — the underwriting workbench — as a competitive advantage. Majority have invested in a homegrown workbench or continue to use disparate tools, avoiding adoption of 3rd party platforms. This remains a greenfield opportunity with no legacy players having truly made the mark. Federato and Sixfold are the two prominent AI-native workbenches.

While the pull for AI point solutions, i.e., non-core workflows is hard to miss today, successful AI-native workbenches may also emerge and take over existing systems of record. Either ways, we’re confident that AI-native workflows will continue to expand the carrier software demand. We're already seeing the leading carriers create net-new budget line items dedicated to AI adoption. And while even the largest incumbents (Guidewire, Duckcreek) couldn’t sweep the fragmented carrier tech stack, tech consolidation is underway. Carriers will soon need to reduce massive spends that go into “running” disparate systems across geographies and lines of business.

Model 2: AI-native broker — making distribution efficient

Insurance sales agents make up the largest wage pool in the insurance value chain — $37B. What the data doesn’t show: for every sales agent, there’s typically a back-office teammate in India or the Philippines keeping broker workflows from falling apart.

You’ve seen Christine’s day. Now compress it into three numbers: ~1 hour per carrier application, sent to up to ~50 carriers when risk appetite is unclear, and hundreds of pages to normalize when carriers respond with quotes.

With that much unstructured data to process, it’s no surprise that Arthur J. Gallagher, one of the largest U.S. brokers, spends 55% of revenue on salaries, with ~20% of its employees based in its Centre of Excellence in India.

The problem is real across all the 40,000 brokers in the US. Yet only the top 100 are sizable, commanding 40% market share, leaving a 60% long tail of sub-10-person shops. Vertafore and Applied Systems — the dominant systems of record, haven’t done a good job at streamling the above workflows. However, competing head-on with incumbents will be inevitable for anyone building a seamless broker experience in the near term.

Meanwhile, as CAC as a percentage of premiums is rising, M&A has become the preferred growth playbook. Tech-enabled roll-ups look promising with the ability to attract larger clientele, unlock better commissions, and deliver ~3× better EBITDA multiples through tech efficiencies. Equal Parts is a recently funded player trying to do exactly this.

Model 3: AI-native Third Party Administrators (TPAs) — streamlining claims handling and assessment

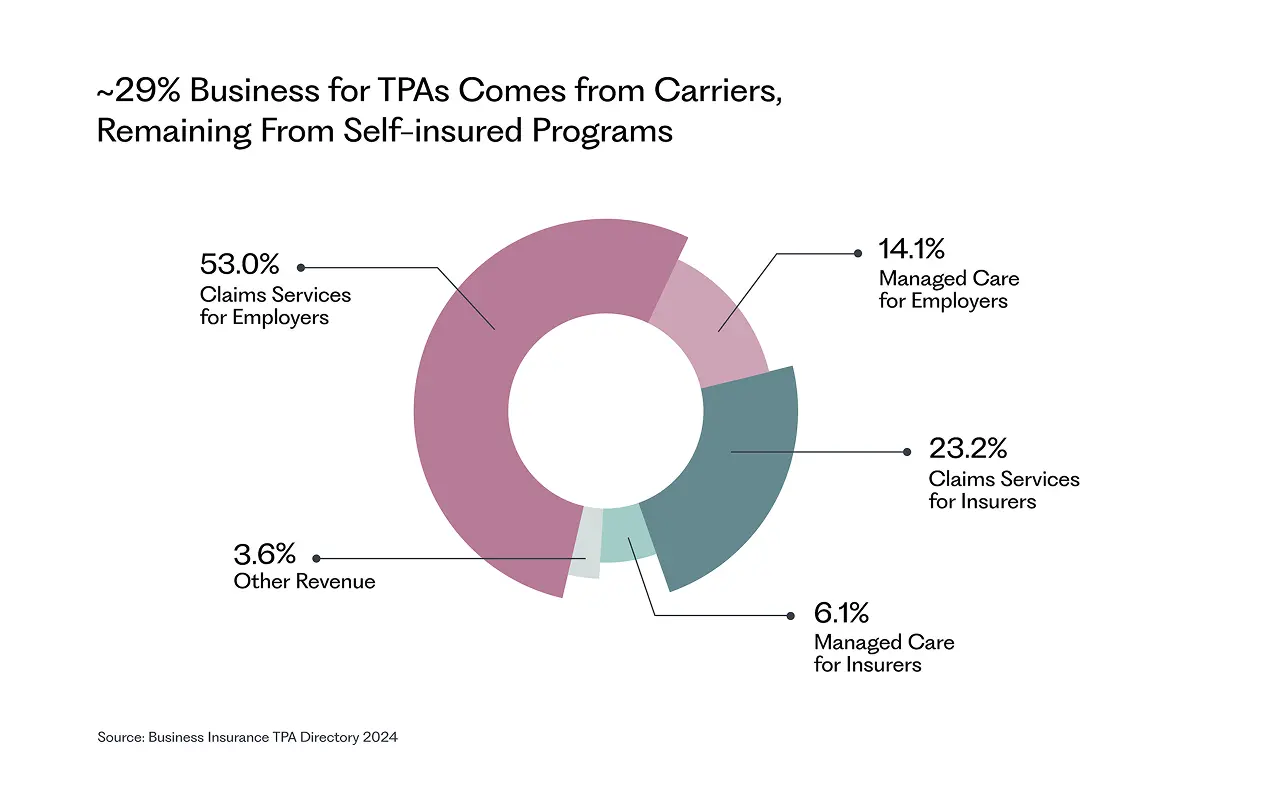

TPAs are a necessary evil in commercial P&C: about 30% of claims are handled by them, the share rising to 43% in workers’ comp and self-insured programs. Carriers lean on TPAs during catastrophes when adjuster demand spikes, and in niche domains where sparse claims volumes don’t justify having in-house specialists. But the sad truth is, TPAs have little skin in the game — they often inflate indemnity and adjustment expenses while delivering poor customer experience.

Why AI-native TPAs make sense:

- Claims sit lower in the pecking order than underwriting; The latter is viewed by carriers as revenue-generating and often attracts higher innovation budget.

- They’re also less “core,” making third-party involvement more acceptable.

- Most of the spend in claims goes to labor, i.e., adjusters, FNOL teams — rather than software, creating room for automation to capture more value.

AI-native TPAs can turn that labor-heavy spend into software-like margins, scaling faster and more efficiently than traditional agentic workflow companies. Reserv, Strala and ClaimsSorted are few names taking this approach.

Insurance AI is another VC-favorite category that has seen $1B+ funding over last 2 years

This space is changing fast, and the best ideas often come from fresh perspectives. If you’re building, experimenting, or even disagreeing — we’d love to connect at [email protected] and [email protected].

We’re looking for the next generation of successful Indian marketplaces. If you’re an early-stage marketplace founder, apply now here or learn more about the #DecodingMarketplaces Startup Hunt.

We’d love to hear about your experiences with marketplaces. Let us share our learnings and build a better and stronger ecosystem. Write to us at [email protected] to be a part of the Accel family.

Subscribe to SeedToScale

/subscribe to get the latest stories from SeedToScale/